The medical products price and tendering-procurement credit rating system, initially established by the National Healthcare Security Administration (NHSA) in August 2020, has undergone a significant evolution. On June 5, 2025, the NHSA introduced the Notice on Further Improving the System of Credit Rating for Medical Products Price and Tendering-Procurement, accompanied by the updated Discretionary Standards and Operational Guidelines for Pharmaceutical Price and Tendering-Procurement Credit Rating (2025 Version) (collectively, the "2025 Guidelines"). These updates aim to further enhance the liabilities of marketing authorization holders (the "MAHs", including the filing/registration entity of the drugs and medical devices) as well as their compliance management obligations to the business cooperation partners, marking a transition toward more rigorous oversight of commercial integrity within the healthcare sector.

A critical development in the 2025 Guidelines is the introduction of Article 7.1.5, introducing a "look-through" mechanism, which addresses scenarios where judicial judgments, administrative penalty decisions, or written determinations identify misconduct (such as commercial bribery) but do not specify the exact products involved and the relevant MAHs or medical institutions. Under this provision, the MAHs of the top three products by transaction volume during the period of misconduct as indicated by the enterprises involved (e.g., distributors) shall assume the consequences of adverse credit evaluation.

Ⅰ. The Impact of Article 7.1.5 in Practice

A notable development in recent months involves the application of Article 7.1.5 of the 2025 Guidelines by certain provincial centralized procurement authorities (the "Procurement Authorities"). We have observed instances where MAHs have received pre-rating notification indicating a preliminary rating of "Serious" or even "Extremely Serious" based on the misconduct of distributors, some of which occurred more than two decades.

An "Extremely Serious" carries severe consequences that can cripple a company's market access. Pursuant to Article 7.1.3 of the 2025 Guidelines, such a rating may lead to the suspension or termination of listing and bidding qualifications for all products under the concerned MAHs within the evaluating province, and simultaneous restrictions on the implicated products' listing and bidding qualifications nationwide.

The recent enforcement challenge associated with Article 7.1.5 arises when criminal judgments mention secondary or tertiary distributors without explicitly indicating the MAHs. Under the 2025 Guidelines, if a Distributor provides evidence identifying a Manufacturer and specific products involved in the misconduct, the Distributor may be credited with "proactive correction" of its own misconduct, shifting the focus of the credit evaluation toward the MAHs. This may lead to the situation where MAHs may be implicated by the disclosures of a downstream entity, even in the absence of a direct contractual or authorization relationship.

Ⅱ. The Importance of Pre-Rating Communication

According to Article 8.3.4, if an MAH takes immediate measures to correct misconduct and eliminate negative impacts upon receiving a pre-rating notification, the Procurement Authorities may refrain from issuing a formal credit rating. Despite the perceived rigor of these new provisions, the 2025 Guidelines provide a critical pathway for regulatory engagement, i.e., the period between receiving a pre-evaluation notice and the issuance of a formal rating. In such cases, capitalizing on the critical window period is essential for enterprises to actively communicate with Procurement Authorities and seek an appropriate approach to mitigate the risk of an adverse credit rating.

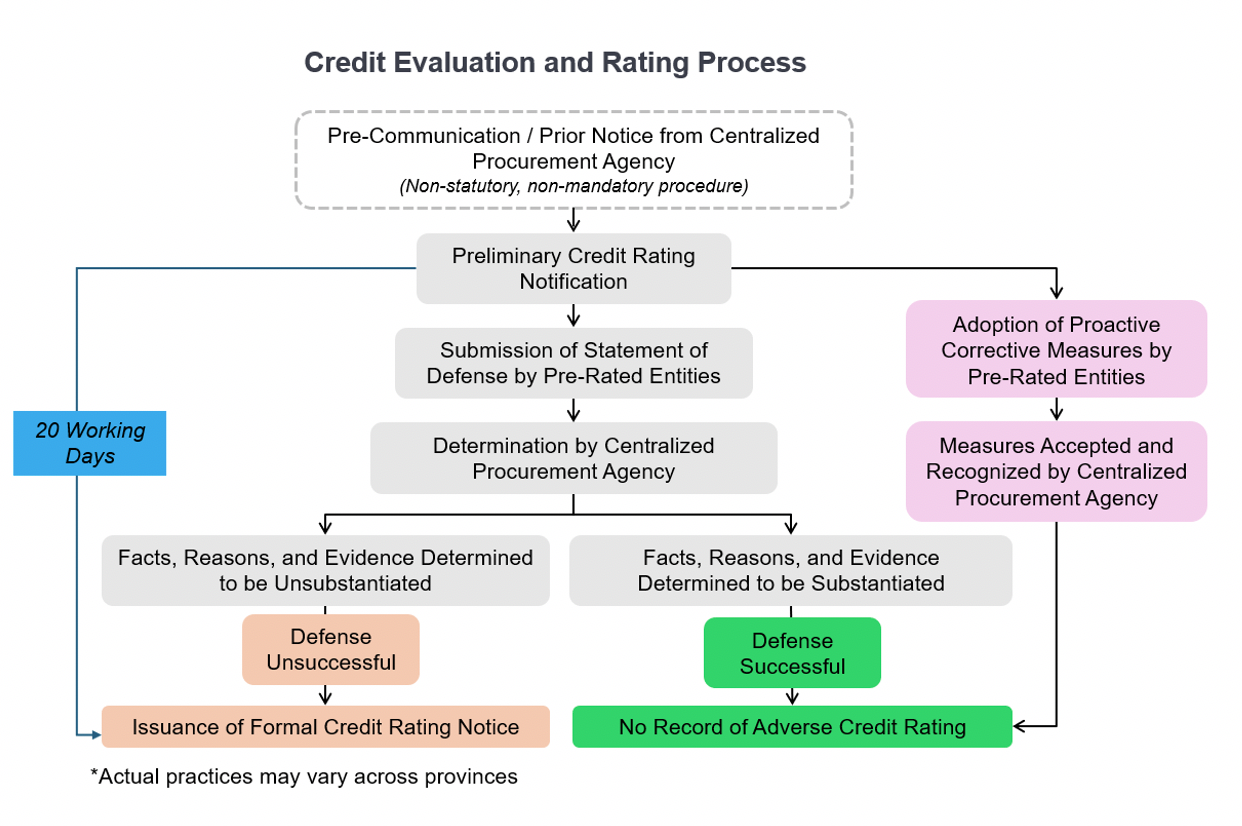

The following flowchart outlines the general procedural path for credit evaluation and rating.

Since the Procurement Authorities in general rely on the legal findings from other authorities (such as judicial judgments, administrative penalties etc.) and do not conduct independent investigations into the underlying facts, the burden of clarification and "proactive correction" measures lie with the MAH. Our recent experience demonstrates that a proactive, evidence-based approach can lead to favorable outcomes. By submitting comprehensive defense letters and supporting materials, clients have successfully achieved "non-rating" results, even when the initial pre-rating notification indicated "Extremely Severe Misconduct".

Ⅲ. Provincial Enforcement Observations and Potential Grounds for Defense

While these observations are drawn from specific provincial practices and do not yet represent a confirmed national trend for the 2025 Guidelines, they highlight critical interpretative discrepancies and potential grounds for defense that concerned enterprises may consider:

-

The "Top Three" Rule: According to Article 7.1.5 of the 2025 Guideline, if the underlying legal document fails to specify products, authorities may identify the top three products by transaction volume (including different specifications of the same generic name) for evaluation of the credit ratings. However, in practice, certain Procurement Authorities may interpret this to mean that the top three products should be determined separately for drugs and medical devices (i.e. a maximum of six MAHs may receive negative credit ratings due to the illegal activities of a distributor as indicated in the legal documents), rather than through a combined ranking of all products; this interpretation would expose a broader range of MAHs to adverse credit ratings, which calls for further clarification from NHSA and legislation authorities regarding the precise evaluation and rating standards.

-

Liability for Vendor's Misconduct: Article 3.3.2 requires pharmaceutical companies to provide a written commitment to assume liability for any dishonest acts committed by their agents or vendors (whether direct or indirect). In practice, however, some Procurement Authorities have applied 'penetration ratings' to MAHs based solely on the fact that a distributor sold the MAH's products to the implicated medical institution, without requiring proof of an actual contractual or agency relationship between the indirect distributors/resellers and MAH. This administrative presumption of agency from the mere act of product sales finds limited support under established principles of civil law and warrants further scrutiny.

Ⅳ. How to Manage Regulatory Communications Prior to Formal Ratings

Upon receiving a pre-rating notification issued under Article 7.1.5, it is recommended that enterprises utilize this critical window period to reinforce their regulatory standing and optimize their internal readiness through the following strategic measures:

-

Comprehensive Information Consolidation: Conduct an extensive data collection to consolidate critical information regarding legal instruments upon which the rating is based, the implicated products, the contractual arrangements, and historical compliance records, etc.

-

Strategic Contingency Planning: Establish a robust response framework that outlines scope of disclosure, refines defense strategies, and prepares personnel through simulation exercises.

-

Cross-Functional Internal Synergy: Strengthen collaboration across departments and enhance internal training on credit rating systems to ensure a unified and efficient organizational response.

-

Proactive Regulatory Engagement: Maintain a cooperative stance with authorities to demonstrate compliance commitment and seek early alignment on remediation procedures and policy requirements

Ⅴ. Closing remarks

The 2025 credit rating system reflects a heightened regulatory focus on the entire supply chain. However, the system also grants enterprises the right to respond to evaluations, present their defense, and request correction of possible misjudgments before any formal negative rating or sanction is imposed. Through proactive, evidence-based communication with authorities during the critical pre‑rating window - a strategy that has enabled our clients to successfully overturn preliminary adverse credit ratings, pharmaceutical companies can effectively manage the risks associated with the "look-through" provisions of Article 7.1.5.