Against the backdrop of global tax governance entering a new era of “look-through regulation”, the revised version of the Common Reporting Standard (“CRS 2.0”) released by the Organisation for Economic Co-operation and Development (OECD) in June 2023 marks a milestone upgrade in the international tax transparency regime. Compared with the original CRS framework, which primarily targeted traditional financial accounts, CRS 2.0 and its subsequent framework documents have horizontally expanded the reporting scope to include emerging digital financial instruments such as crypto-assets, electronic money products, central bank digital currencies, and real estate; vertically, the rules have strengthened “look-through” identification requirements for individuals holding multiple tax residencies and for the ultimate beneficial owners of offshore structures.

Among the most significant changes is the closing of loopholes in the reporting rules applicable to dual tax residency status. Under prior practice, the commonly adopted “choose-one jurisdiction reporting” approach is no longer acceptable. CRS 2.0 now requires account holders to truthfully report all jurisdictions in which they are tax residents, and financial institutions shall simultaneously exchange the relevant account information with all corresponding tax jurisdictions. This fundamentally eliminates the institutional loophole of avoiding information exchange through identity switching.

Driven by these rule upgrades, Hong Kong, as a major international financial center, submitted the Inland Revenue (Amendment) (Automatic Exchange of Information) Bill 2026 (“HK CRS 2.0”) to the Legislative Council on April 1, 2026, with the amendments expected to take effect on January 1, 2027. Although HK CRS 2.0 does not expressly introduce a new substantive obligation requiring taxpayers to truthfully declare all jurisdictions of tax residence—such requirements have already been embedded in the existing CRS self-certification forms and in the due diligence procedures of Hong Kong financial institutions—the Bill substantially enhances the rigidity and deterrent effect of enforcement by significantly increasing penalties in a systematic manner.

Owing to its simple tax system, limited categories of taxes, and comparatively low tax rates, Hong Kong has long served as a core jurisdiction for cross-border identity planning among high-net-worth individuals from Mainland of China. With the increased granularity of information exchange and enhanced enforcement efficiency brought about by CRS 2.0, a fundamental question is becoming increasingly clear: which country are you actually a tax resident of?

This article aims to systematically examine the rules governing the determination of tax resident individual in Mainland of China (hereinafter “China” or the “Mainland”; for purposes of this article, excluding the Hong Kong and Macau Special Administrative Regions and Taiwan) and the Hong Kong Special Administrative Region (“Hong Kong”). Through practical scenarios involving individuals living between both regions, this article further illustrates the application of the “tie-breaker rules” in cases of dual tax resident, with a view to providing a reference framework for high-net-worth individuals restructuring their compliance arrangements in the era of CRS 2.0.

I. Determination Criteria and Factors for Consideration for Mainland Tax Resident Individual

Under the provisions of the Individual Income Tax Law of the People's Republic of China (2018 Amendment) and its Implementing Regulation, a Mainland tax resident individual refers to an individual who either has a domicile in China, or who does not have a domicile in China but stays in China for an aggregate of 183 days or more within a tax year. “Having a domicile in China” refers to habitually residing in China by reason of household registration, family ties, or economic interests.

As can be seen from the above provisions, China applies two criteria for determining tax resident individuals: the “stay days” criterion (183 days) and the “domicile” criterion. Satisfaction of either criterion is sufficient for an individual to be classified as a Mainland tax resident. Among these, the “stay days” criterion is relatively straightforward, whereas the “domicile” criterion mainly focuses on whether the individual habitually resides in China. The concept of “habitual residence” provides only several reference factors—namely household registration, family ties, and economic interests—and in practice depends heavily on a holistic assessment of the factual circumstances. For example:

-

Individuals residing overseas for purposes such as study, employment, family visits, or travel, who return to reside in China after the relevant purpose ceases to exist, may be regarded as habitually residing in China.

-

Conversely, where a foreign individual resides in China solely for temporary purposes such as study, employment, family visits, or travel, and returns overseas once those purposes cease to exist, such individual will generally not be regarded as habitually residing in China, even if he or she has purchased a residential property within China.

-

According to a publicly available case, a foreign individual was determined to have closer economic interests connected with China and was therefore regarded as habitually residing in China. In that case, there was no clear indication that the individual resided overseas, and accordingly the individual was classified as a Mainland tax resident.[1]

Based on the current rules and publicly available cases, we understand that the concept of “habitually residing in China” implies a degree of permanence and long-term continuity, rather than a location used merely for short-term or temporary stays or for purchasing assets. For foreign individuals, where their purpose for coming to China is temporary in nature—such as study, employment, or family visits—and they will return overseas once the relevant purpose ceases, their habitual residence is generally not considered to be in China. However, where a foreign individual has established deep and continuous economic, social, and family connections with China, and there is no clear indication that the individual resides overseas, Chinese tax authorities may in practice determine that the individual’s habitual residence has shifted to China, thereby rendering the individual a Mainland tax resident. The same reasoning may likewise apply to Chinese individuals.

II. Determination Criteria and Factors for Consideration for Hong Kong Tax Resident Individual

Under the Hong Kong Inland Revenue Ordinance, “resident for tax purposes— (a) in relation to Hong Kong, means— (i) an individual who ordinarily resides in Hong Kong; (ii) an individual who stays in Hong Kong— (A) for a period or a number of periods amounting to more than 180 days during a year of assessment; or (B) for a period or a number of periods amounting to more than 300 days in 2 consecutive years of assessment if one of the years is the year of assessment concerned;…”. Accordingly, the determination of Hong Kong tax resident adopts either the “ordinarily resides” criterion or the “stay days” criterion.

These criteria are similar to those of Mainland of China. The “stay days” criterion (180/300 days) is relatively clear and objective, whereas the “ordinarily resides” criterion constitutes a more complex factual determination that requires case-by-case analysis.

Based on our review of the rules published on the website of the Hong Kong Inland Revenue Department, official FAQs, as well as more than twenty judicial decisions issued in recent years[2], the core principles underlying the “ordinarily resides” criterion may be summarized as follows:

-

Generally, if an individual maintains a permanent home in Hong Kong for use by himself or his family as a place of living, he will be regarded as “ordinarily” residing in Hong Kong. Other relevant factors include the number of days spent in Hong Kong, whether the individual maintains a fixed place of residence in Hong Kong, whether he owns residential property overseas, and whether he primarily resides in Hong Kong or elsewhere.

-

The “ordinarily resides” criterion requires that the individual’s residence status in Hong Kong possess a certain degree of continuity, habituality, and regularity, and that such status is not interrupted by occasional or temporary absences from Hong Kong.

-

The determination of “ordinarily resides” falls within the scope of factual and degree judgment, based on objective historical facts, rather than on future intentions or expectations of residence that carry implications of permanence.

For example, where an individual is assigned by a Hong Kong employer to work in Mainland on a long-term basis but will return to Hong Kong upon completion of the assignment, that individual may still be regarded as ordinarily residing in Hong Kong. In contrast, an individual who merely owns rental property in Hong Kong and returns only for a few days each year would generally not be regarded as ordinarily residing in Hong Kong.

Based on our experience, the above criteria applied in Hong Kong are broadly similar to those in Mainland in that both are fact-based and emphasize actual living arrangements as well as life and economic connections. Nevertheless, there remain notable differences between the two regions in terms of the weighting and degree judgement of various factors.

III. Tie-breaker Rules under the Tax Arrangement between Mainland and Hong Kong

Due to the differences between Mainland and Hong Kong in their respective tax resident determination criteria, it is possible for the same individual to be simultaneously regarded as a tax resident by both jurisdictions, thereby resulting in “dual tax resident”. Pursuant to Article 4(2) of the Agreement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Incomes (“CN-HK Tax Arrangement”):

“2. Where by reason of the provisions of paragraph 1 an individual is a resident in both Contracting States, then his status shall be determined as follows: (1) He shall be deemed to be a resident only in the State in which he has a permanent home available to him; if he has a permanent home available to him in both States, he shall be deemed to be a resident only in the State with which his personal and economic relations are closer (‘centre of vital interests’); (2) If the State in which he has his centre of vital interests cannot be determined, or he has not a permanent home available to him in either State, he shall be deemed to be a resident only in the State in which he has an habitual abode; (3) If he has a habitual abode in both States or in neither of them, the competent authorities of the Contracting States shall settle the question by mutual agreement.”

The above rules under the CN-HK Tax Arrangement are commonly referred to as the “tie-breaker rules.” In other words, where an individual constitutes a dual tax resident of both Mainland and Hong Kong, his or her tax residency shall be determined sequentially according to the following criteria: permanent home (or “permanent domicile”)→centre of vital interests (i.e., the jurisdiction with closer personal and economic connections)→habitual abode (or “habitual residence”)→settlement by mutual agreement between the tax authorities of both parties. According to the relevant rules, the factors considered under each criterion include:

-

The “permanent home” includes any form of residence, provided that it possesses a degree of permanence, rather than being used merely for temporary stays for purposes such as traveling or business visits.

-

The “centre of vital interests” requires a comprehensive assessment of the individual’s family, social, and economic connections, with particular emphasis on the individual’s actual life trace. In general, the jurisdiction where the individual consistently lives, works, and maintains family and property connections is regarded as the individual’s centre of vital interests.

-

The “habitual residence” primarily focuses on the amount of time spent in each jurisdiction.

IV. Practical Cases of Cross-Border Life — From the Perspective of Tax Authorities in Two Regions

1. Two public cases in Mainland

Case 1 [3] :

In 2013, Mr. S entered into an employment contract with Company C, a Mainland company. Under the contract, his principal place of work was a city in Mainland. Company C paid his salary and made social insurance and housing provident funds contributions on his behalf. Mr. S owned three self-occupied residential properties in that Mainland city and actually resided in one of them.

Since 2014, Mr. S had concurrently served as an executive director of Company D, a Hong Kong subsidiary of Company C, and also performed duties in Hong Kong. No mandatory provident fund contributions were made for him in Hong Kong. For work convenience, Mr. S leased and continuously resided in a residential property in Hong Kong. In 2014, both Mr. S and his wife obtained Hong Kong resident status, and their child attended school in Hong Kong. The Hong Kong tax authorities issued certificates of resident status to Mr. S for 2014 and 2015.

In this case, the Mainland tax authorities applied the tie-breaker rules to determine Mr. S’s tax residency status. Based on the conclusion that his centre of vital interests was located in Mainland, he was ultimately determined to be a Mainland tax resident.

Case 2 [4] :

Mr. Y held Mainland household registration and the identity card, and obtained Hong Kong permanent resident status in 2018. Mr. Y owned and worked for a partnership enterprise in Mainland, where he also paid social insurance and individual income tax on employment income. In addition, Mr. Y’s spouse and children had long resided in Mainland for work and education purposes.

At the same time, Mr. Y was employed by a Hong Kong company, from which he derived employment income, and in Hong Kong he paid salaries tax and mandatory provident funds. During the relevant years, Mr. Y’s period of residence in Mainland did not exceed 183 days, and his stay in Hong Kong also did not exceed 180 days.

Similar to Case 1, the Mainland tax authorities in this case concluded that Mr. Y’s family and economic interests were more closely connected with Mainland, and therefore determined that he was a tax resident of Mainland.

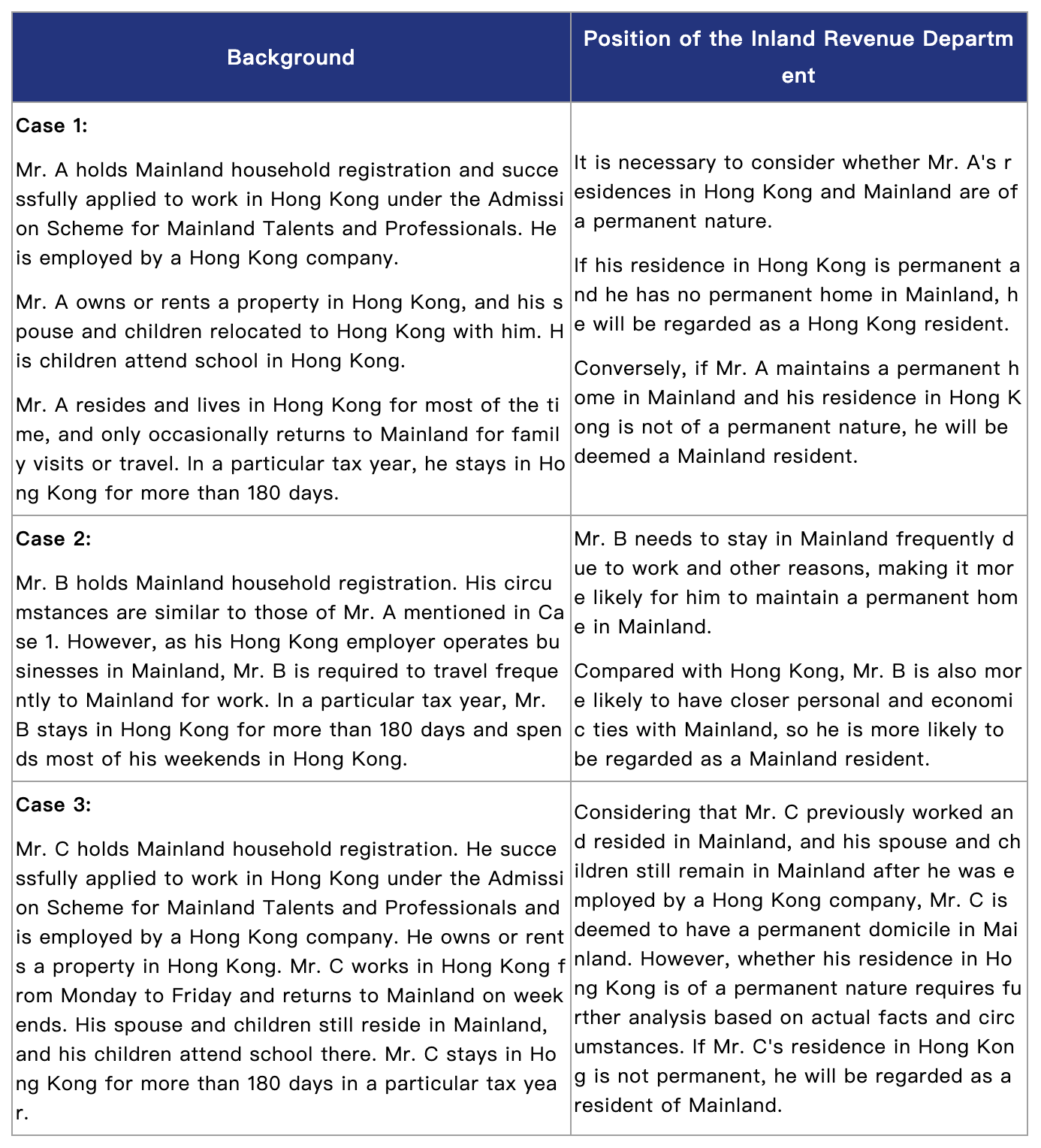

2. Latest Cases Published by the Inland Revenue Department of Hong Kong

The website of the Inland Revenue Department updated a series of General Matters and Frequently Asked Questions concerning the tie-breaker rules on December 22, 2025, which to some extent reflect the Hong Kong tax authorities’ enforcement position toward such rules. In particular, the discussions of several cases closely resemble real-life situations and therefore merit further attention:

3. Tax Insights into the Cross-Border Life Between Mainland and Hong Kong

Based on the above cases, the following implications are particularly noteworthy for high-net-worth individuals maintaining a “cross-border life” between Mainland and Hong Kong or other jurisdictions:

(1) Overseas identity is not equivalent to tax residency status: Possessing foreign permanent residency or overseas identity does not necessarily mean that an individual is no longer a tax resident of Mainland (nor does it automatically equate to being an overseas tax resident).

(2) Physical presence is not a “safe harbor”: Meeting the Hong Kong “stay days” threshold associated with the “ordinarily resides” criterion (such as 180/300 days) does not constitute a safe harbor for Hong Kong tax resident. The tax authorities of both regions may still make further determinations based on the “ordinarily resides” or “domicile” tests.

(3) Mainland household registration remains highly influential: For Mainland citizens, even where they work or reside overseas for extended periods, the retention of Mainland household registration and a Chinese identity card may still lead the tax authorities to classify them as Mainland tax residents under the “domicile” test. In practice, this criterion operates independently of, and may carry greater weight than, the “stay days” criterion.

(4) The permanent home criterion is objective in nature: The determination of a permanent home is based on objective living facts rather than solely on an individual’s subjective intentions or future plans.

(5) The centre of vital interests is the key determining factor: In “cross-border life” situations—where an individual maintains residences and activities in both Mainland and Hong Kong—the location of the individual’s centre of vital interests (including family, social relations, principal assets, and business activities) constitutes the core basis upon which Mainland tax authorities determine whether the individual is a Mainland tax resident.

V. Conclusion

The determination of an individual’s tax residency status is both a complex and dynamic issue. Formal identity can no longer serve as an absolute standard for determining tax resident. Both an individual’s recent work and living arrangements, as well as long-standing personal and economic connections, may affect the ultimate determination of tax residency status.

On April 1, 2026, the press conference of the State Taxation Administration clearly signaled that the tax authorities would utilize CRS cross-border financial account information to conduct rigorous verification and analysis of offshore income reporting data. Against this backdrop, the determination of tax residency status, the compliant reporting of offshore income, and the reshaping of offshore structures are no longer matters confined to the application of rules within a single jurisdiction. Rather, they involve the interaction between the tax laws and tax arrangements of both Mainland and Hong Kong, together with the increasingly complex overlap of CRS rules.

Amid the continuing rise in global tax transparency, individuals and family-owned businesses can no longer effectively respond to increasingly sophisticated and dynamic compliance requirements merely by obtaining foreign identities or opening accounts in non-CRS participating jurisdictions. Traditional "tax haven" planning is no longer sustainable. High-net-worth individuals should shift toward constructing a "tax compliance stronghold" to effectively mitigate legacy risks and achieve long-term tax compliance in an era of CRS transparency.

[1] Fenglin Tang compiles: International Tax Case Collection, "Case 1-1: Xiamen Tax Authorities' Determination of Tax Residency Status Through the Application of the Tie-Breaker Rules."

[2] Including cases for judging the "ordinarily resides" criterion under the rules governing application for Hong Kong tax resident and Personal Assessment.

[3] International Taxation Department of the State Taxation Administration compiles: Case Collection on the Implementation of Tax Treaties, "Case 1: Accurately Determining Individual Tax Residency Status by Applying the 'Tie-breaker Rules'."

[4] China Tax News: Application of the "Tie-breaker Rules" to Determine Tax Resident Identity, published on December 5, 2025, by Zhewei Wang (Affiliation: Tianjin Municipal Tax Bureau of State Taxation Administration).